Sign up for Funding Circle newsletter!

Get our latest news and information on business finance, management and growth.

United States

United States

Updated: March 27th, 2020

It’s no secret that, at Funding Circle, we have our fair share of finance junkies. We love to get lost in the jumble of terminology and metrics that permeate our industry. But we know that most businesses looking for financing don’t have time to wade into the deep end with us—you’re busy running and growing your business!

To help you make a more informed decision about financing, we’ve broken down the three key terms of a small business loan: principal, interest and fees.

Principal is a fancy name for the amount of money you have borrowed and have yet to pay back.

If Sam lends Jake $100 on Monday, the principal is $100. If Jake pays Sam back on Tuesday with $20 he finds in his jacket pocket, the remaining principal is $80.

Like the principal of a middle school, your loan principal determines how the other parts of your loan function. Interest and fees are often given as a percentage of the principal, so this is the first number to establish and consider when trying to understand the terms of a loan.

Interest is the amount of money a borrower pays the lender in exchange for the privilege of using their money. You can think of it as the amount you pay to “interest” the lender into giving you a loan.

Interest can be simple:

Sam lends Jake $100 with 10% interest on Monday, so Jake owes Sam $110 when he pays him back at the end of the week.

Or interest can be compounding, which means you pay interest on top of the interest you already owe:

Sam lends Jake $100 on Monday with 10% interest, compounding daily. If Jake repays the loan in full on Tuesday, he’ll owe $110. However, if he doesn’t repay the loan until Wednesday, he’ll owe $121: $110 + ($110 x 10%).

It’s important to remember that the higher the number of compounding periods (eg. daily, weekly, monthly, annually), the higher the compound interest. For example, the amount of compound interest you’ll owe on $100 compounded at 10 percent annually will be lower (cheaper!) than if it compounded at 5 percent bi-annually.

Depending on who you borrow money from, you may be presented with various fees that can substantially increase the cost of your loan. These fees fall into two buckets—fees that are charged upfront or at “origination,” and fees charged over the life of the loan.

An origination fee is a simple, one-off fee lenders charge to cover the cost of evaluating and originating your loan. At Funding Circle, your origination fee will range from 3.49% to 6.99% of the total amount you borrowed and is based on the strength of your credit profile. It is deducted from your total loan proceeds, which means you do not pay this fee if you do not receive a loan.

Some lenders (but not us!) tack on a slew of additional initial fees for things like submitting an application, processing the loan, preparing the documents or underwriting the loan.

If you’re borrowing from another lender, you should also be on the lookout for ongoing fees. These fees are incurred during the life of your loan or when you pay it back. Many lenders also charge a prepayment penalty fee to discourage borrowers from paying off their loan early. Using our previous example, it would look something like this:

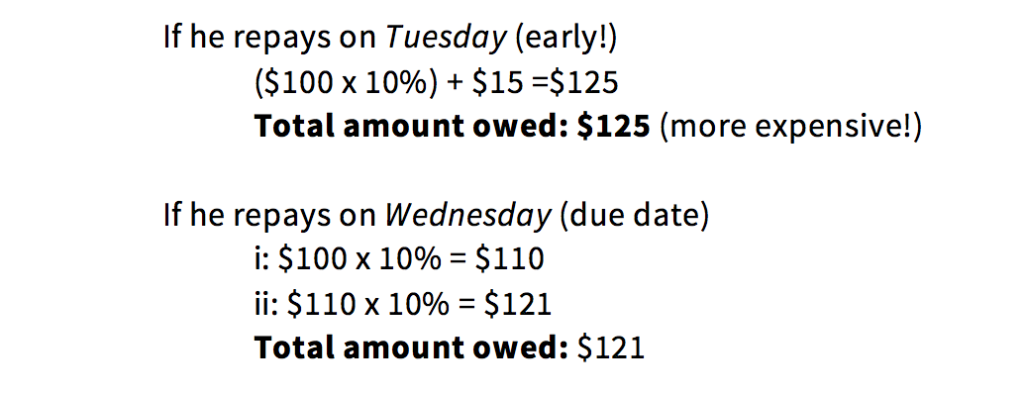

Sam lends Jake $100 on Monday with 10% interest, compounding daily and a prepayment penalty of $15. The loan must be repaid by Wednesday. If Jake had $110 on Tuesday, he could pay back Sam early and avoid paying additional interest (saving $11!). However, because he agreed to a loan with a prepayment penalty, he would actually have to pay $125. The prepayment penalty allows Sam to earn more money on interest by encouraging Jake to wait until Wednesday to pay off the loan.

At Funding Circle, we don’t think that’s fair. We will never penalize you for paying your loan back early.

Just looking at the basic components of a loan, you can see how quickly things can get complicated—which is why it’s so important to work with a lender who has your best interests at heart.

At Funding Circle, we believe all business owners deserve the right to transparency. That’s why we partnered with other industry leaders to set the first-ever gold standard for responsible business lending in America: The Small Business Borrowers’ Bill of Rights. We promise to always disclose rates and fees upfront and in plain-English, so you never have to worry about hidden costs.

Once you’re ready to compare loan offers, it’s helpful to have a single number that brings together the key components of each loan you’re considering. That number is known as an Annual Percentage Rate (APR), and a good lender will always be willing to help you calculate it.

You deserve to work with a lender who empowers you with the knowledge you need to make the best possible financing decisions for your business. Check your eligibility today for a small business loan with Funding Circle.

Louis DeNicola is the president of LD Money Media LLC and an experienced finance writer who specializes in credit, personal finance, and small business finance. Within the small business sphere, he helps business owners understand their financing options, cash flow management, business credit, and taxes. In addition to Funding Circle, you can find his work on BlueVine, Credit Karma, Experian, Wirecutter, and Lending Tree.

Get our latest news and information on business finance, management and growth.