-

United Kingdom

United Kingdom

- Sign in

United Kingdom

Updated: 9 September 2021

Jerome Le Luel is the Global Chief Risk Officer of Funding Circle. He leads a team of more than 100 risk professionals including data scientists, risk analysts and credit assessment experts. Jerome joined Funding Circle five years ago, bringing with him more than 20 years of experience in risk management. His previous roles include Global Head of Risk Analytics at Barclays Bank and Global Chief Risk Officer at Barclaycard, where he successfully navigated their global portfolio through the 2008/9 recession.

As the summer draws to a close and we reflect on the changes since my last update in March, we can see signs of sustained progress in many aspects of the economic recovery. The success of the vaccination rollout has allowed trading restrictions to be relaxed, helping businesses welcome back customers and increase their activity.

We are both hearing and seeing a positive picture from the many business owners we speak to, as they begin to look to the future and take opportunities to grow as the country reopens. In a survey we carried out with the British Chambers of Commerce, we found that 63% of small businesses are confident in their growth prospects over the next 12 months, with 80% expecting to be operating at pre-pandemic capacity by October.1

Although there is some welcome news, a level of uncertainty still remains. The furlough scheme comes to an end this month, some sectors continue to be affected, and the full impact of reopening schools, offices and events at full capacity is yet to be seen. However, overall the data suggests that the current health of small businesses is more positive than was initially feared.

In this update I’ll look at some of the data in more detail, as well as looking at how businesses have stayed on track with their loans and how this will affect your returns. The key points include:

Faced with a changing environment, businesses have been through several peaks and troughs over the last 18 months. We can see this in the graph below, which looks at the average change in turnover experienced by businesses on our loanbook since the pandemic began.

To begin with we can see initial drops and fluctuations as restrictions came in, followed by a more stable, positive period last summer. There was a 12% drop again during the January lockdown, but as restrictions were eased once more businesses saw a sharp increase in turnover between February-April, and it has remained stable in the months since.

This return to stability is welcome news for all, and we have seen positive signs across the board. We can see this in the graph below, which uses credit and debit card data to look at the amount spent on different categories of purchases.

Spending on ‘Staples’ (food & drink, utilities) has remained consistent throughout the pandemic, while ‘Work related’ goods (commuting, fuel) is back to pre-Covid levels. Although ‘Delayable’ (vehicles, clothing, luxury, recreational goods) and ‘Social’ purchases (hotels, non-commuting transport, hospitality) are still below their pre-pandemic levels, they have recovered significantly in recent months.

This shows that, as expected, businesses in some industries will be faring better than others. Overall however, businesses in all of the above categories are showing positive signs and the outlook continues to improve.

Data provided by the Office for National Statistics. More information on the methodology behind these categories can be found in this article by the Bank of England.

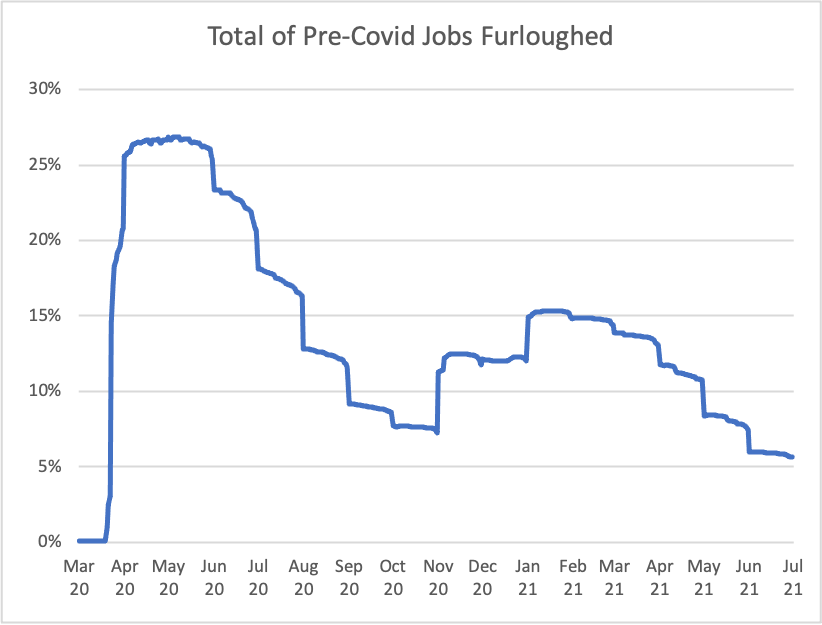

Businesses are also coping well with the tapering down of government support such as the Furlough Scheme. Introduced to help prevent job losses, as trading restrictions have been eased, the scheme has been reduced in stages, and is due to end on 30th September.

Up to now businesses have been largely successful in retaining employees as the scheme has been phased out. The redundancy rate returned to pre-pandemic levels and there were 953,000 job vacancies in May to July 20213, a record high.

However, 6% of jobs are currently still supported through the scheme, representing over 1.8 million people, and it remains to be seen how the ending of the scheme will affect these roles.

Data from HMRC statistics on the Coronavirus Job Retention Scheme

Along with the factors mentioned above, the improving economic environment is reflected in recent growth figures, with GDP growing by 4.8% between April and June4. Small businesses are central in driving that recovery, and we’ll continue to support them as they look to grow in the wake of the pandemic.

I have discussed in previous updates the resilience and determination that small businesses have shown throughout the pandemic, and we continue to see this in the businesses you have lent to.

After the initial increase in businesses asking for payment plans, the measures we took to support them along with stimulus from the government, helped them continue to trade and get back on their feet. As a result, the vast majority began repaying as their plans came to an end. 98% are now making repayments, up from the 95% we saw in March.

Although government support is now being tapered down, the number of businesses missing a first repayment has remained stable at pre-Covid levels for over a year. This can be seen across sectors. As shown in the graph below, the Arts, Entertainment, Leisure and Hospitality sectors were among the worst affected when the pandemic began, but recovered by July last year and have remained stable since.

Since our last update, we have used the latest available data to refine our estimates for projected lifetime returns. You can see the updated returns by cohort of loans below.

Overall I’m pleased to say that we still expect returns to stay positive and, even if we remain cautious about the future outlook, most cohorts have improved since our March 2021 estimates, thanks to more businesses being able to repay than initially anticipated. As time goes by and the loans are repaid, the volatility of this forecast is also reducing, giving us more confidence in these estimates. However, as expected during a recession, returns are lower than initially forecast.

| Loan cohort | Projected Returns – March 2021 | Updated Projected Returns |

| 2015 | 6.6% – 6.7% | 6.6% – 6.7% |

| 2016 | 4.5% – 4.9% | 4.7% – 5.1% |

| 2017 | 2.8% – 3.3% | 3.3% – 3.8% |

| 2018 | 1.3% – 2.3% | 2.0% – 3.0% |

| 2019 | 1.2% – 2.7% | 2.1% – 3.1% |

| 2020 | 2.2% – 4.0% | 4.5% – 5.5% |

We continue to provide small businesses with access to finance through the Government’s new Recovery Loan Scheme, alongside lending through Funding Circle’s existing commercial loan product. As retail investors are not able to participate in government-backed loans, lending remains paused. Applications for the Recovery Loan Scheme are currently open until the end of 2021. Following this, we will review lending for retail investors.

The improvements seen both in our own loanbook performance and the growth seen in GDP and employment, all help to show an improving outlook for the economic recovery. However, with uncertainty remaining we will stay vigilant, with careful monitoring of loan performance and the wider environment.

We will keep working with businesses to get the best outcomes both for them and the investors who lent to them, and, as always, we thank you for your support as we continue to respond to the unique challenges created by the pandemic.

All data is from Funding Circle unless otherwise stated

5779 REVIEWS