6th August 2026

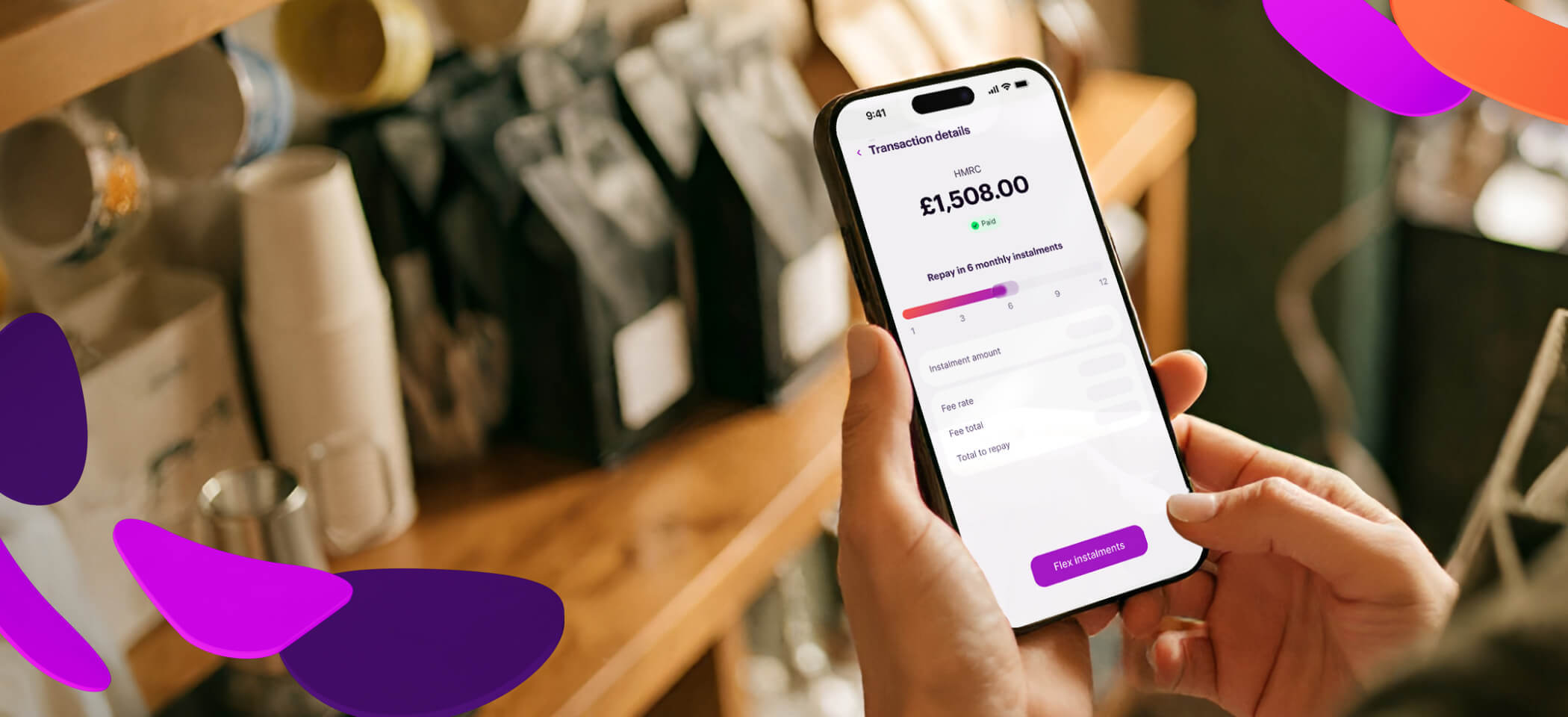

Your business, in your pocket: work and pay your way with the new Funding Circle app

News

29th July 2026

What is alternative finance? Options for UK businesses

Business Finance

29th July 2026

High limit business credit cards UK

Business Finance

28th July 2026

Late payments: your rights and how to chase them

Business Finance

27th July 2026

How to reduce business costs

Business Finance

26th July 2026

Visa vs Mastercard: what is the difference?

Business Finance

Resource Centre

Go further with our videos, guides, news and more

Learn more about our business loans and business credit card products